Zoom! Part II

At what price Zoom ... Biden Lowers Gas Prices ... Results: UP .7%; vs S&P DOWN (5%)

Zoom (ZM)

I started writing about ZM last week. During the pandemic, the price zoomed 😊 to the stratosphere. Now, something like Newtown’s Third Law of Motion has kicked in and the price is down 68% this year. Is it a good time to buy? At what price is it a good investment?

Before I get to that. There is good news on the inflation front. Gas prices here in eastern Pennsylvania have dropped from $4.99 a gallon down to $4.75.

I attribute that to President Biden’s inspirational and evolving leadership:

When entreaties to Vlad the Inflator didn’t work the president pivoted.

That didn’t work either. But you know, when you fall off your horse (or your bike) you just have to climb back on.

On July 2nd the President took to Twitter and finally found his voice!

Success! Read the real tweet here:

ZOOM

To recap from last week, Zoom, pre-pandemic, was a business-to-business provider of communication services. During the pandemic the company’s value soared as the video conferencing service became popular among consumers. Now the price has fallen to earth and Zoom has gotten back to business.

Last week’s newsletter on Zoom is here:

So, what does the future hold for Zoom and at what price is it a ‘buy’?

The Market

In a March 1, 2022 research note, Morningstar analyst Dan Romanoff pegs market size for the “collaboration software market” at $100b.

“Zoom is one of the leading names in the unified communications and collaboration (UC&C) space, which is expected to witness a healthy CAGR of 27.8% during 2020-2025 period”[1]

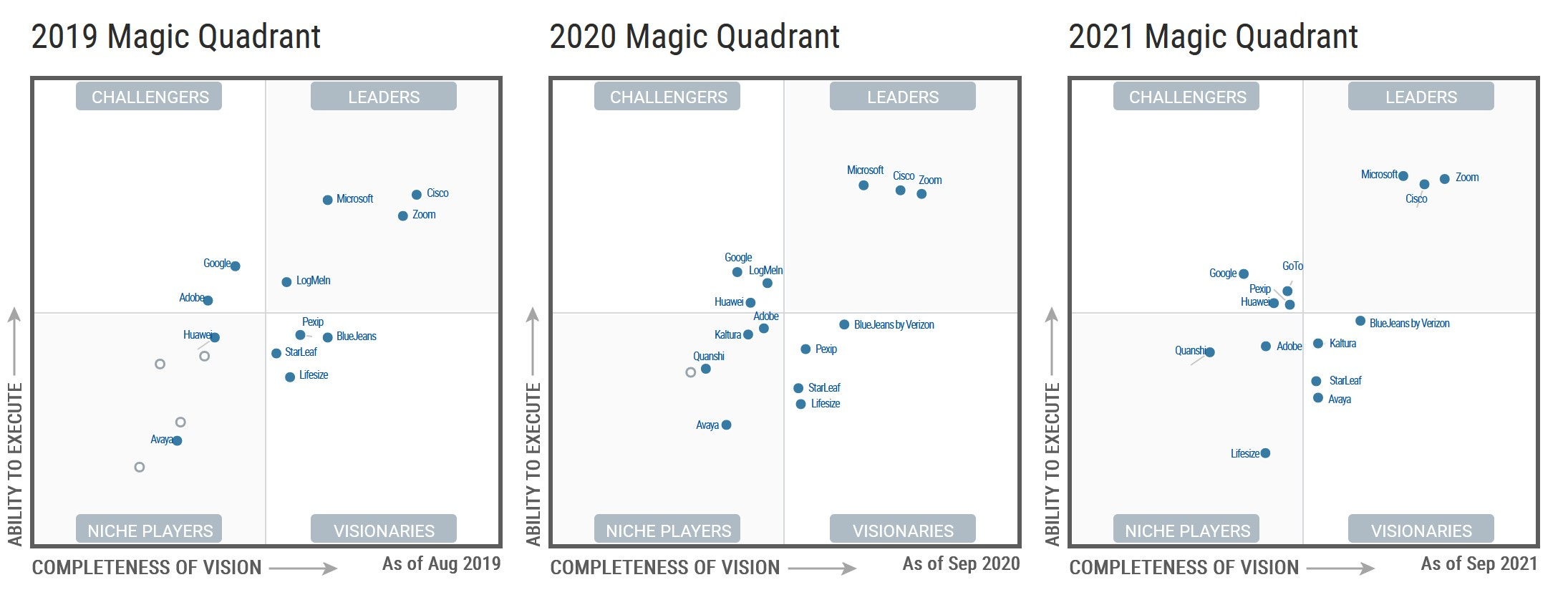

Market leadership, for the past three years, hasn’t changed much. [2] Microsoft, Cisco and Zoom dominate.

In a very large and growing market, Zoom shares a stable leadership position with Microsoft and Cisco.

Zoom is the low-price leader with a strong cross sell/up sell strategy to increase revenue per customer. What’s that worth if, like me, you have a ten-year investment horizon?

Ten years is long, long time; here’s where I think this goes between now and 2033.

Assumptions

Based on what I read in the 10ks, 10Qs and the earnings call transcripts, I’m thinking this.

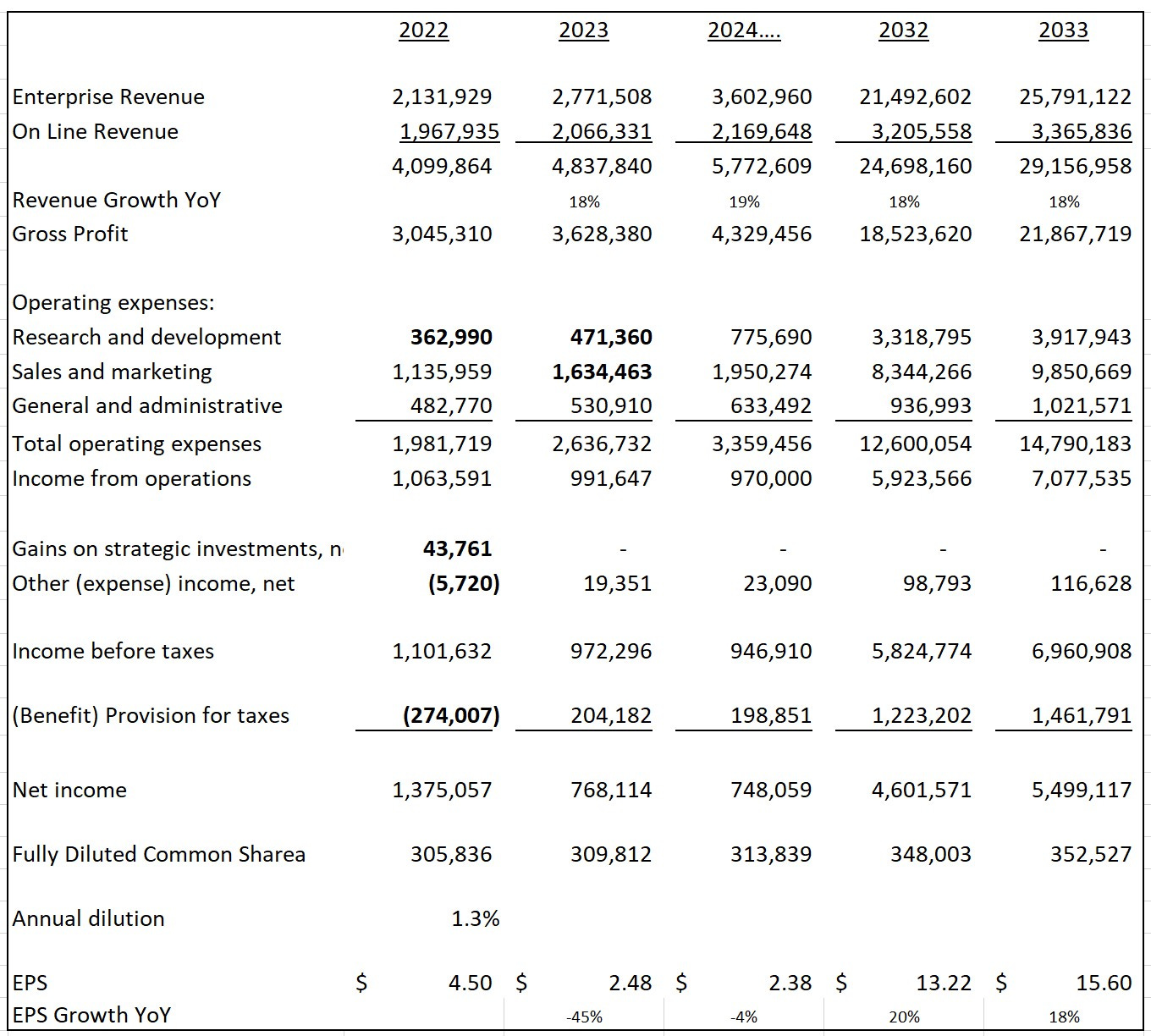

Enterprise revenue will continue to grow well (30%+ per year) in the near term and then slow down into the 20% +/- range in the out years. Revenue from the small business and consumer ‘on-line’ segment will be flattish. Overall revenue growth will be in the high teens, low 20% range.

R&D expenses will consume a greater % of revenue as the company’s cost advantage in China fades. Sales and marketing to enterprise customers will increase costs compared to what the company enjoyed during the pandemic.

One-time benefits like “gain on strategic investment” ($43m in 2022) and negative “other expenses” ($5m in 2022) won’t bolster earnings per share.

Don’t forget taxes. The company has used most of its NOL’s. I’m baking in roughly 20% effective tax rate.

Zoom P&L Model - 2022 to 2033

“It’s hard to make predictions, especially about the future” ~ Yogi Berra

Dilution from employee stock compensation seems to have decelerated in the past two years. In my model I’m assuming it drops from the 2.6% per year that investors have suffered over the last two years to 1.3%. That’s just a guess.

Summary

All this (if true) gets $15.60 per share in earnings in 2033. At 22X earnings – that’s a $343/share ten years from now with a present value of $147.

I look for a 40% margin for error with shares I buy – so my price is about $89. The stock closed at $119.80 on Friday. I’ll watch and wait on this one.

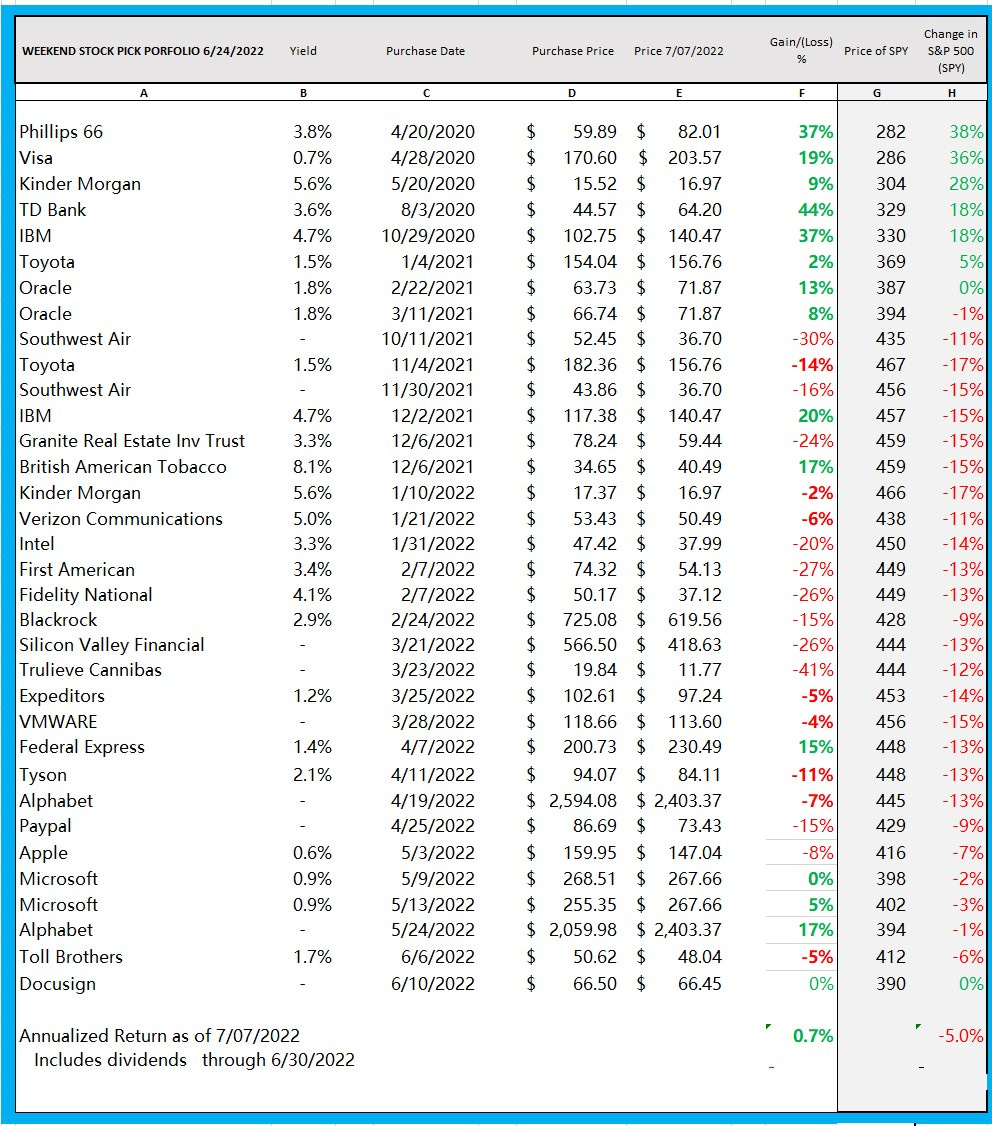

Portfolio Results:

Portfolio: Up 0.7 % vs. S&P 500: Down 5.0%

This is the 26th month of a 120-month project.

The project tests a theory that, over ten years’ time, a “buy low, sell never” portfolio of stocks bought at a discount to their estimated present value will both make money on an absolute basis and outperform the S&P 500

The portfolio has gained 0.7% annualized and including dividends since April of 2020.

Investments in the SPDR etf SPY over the same period of time have lost 5% annualized (including dividends).

22 of the 34 purchases have performed better than the ETF (SPY) over the same period of time.

This is what it looked like when the market closed on Friday.

I was a little late publishing this weekend’s edition - blame it on very nice weather at the beach.

Thanks for reading. If you like this please share. Subscriptions are free.

Or email me at: weekendstockpick@gmail.com and check out my website

https://www.weekend.financial/

[1] Zacks Research, June 27, 2022

[2] Gartner; Magic Quadrant for Meeting Solutions, October 7, 2021