Phillips 66 (NYSE: PSX)

Looks more like Phillips 65 to me. And how is inflation like a Jack in the Box?

Oversold: PSX Phillips 66.

PSX operates refineries, pipelines and retail locations. The company recently announced what amounts to a restructuring and simplification of the business. The company is buying out the publicly held shares of PSPX, a MLP in their pipeline business.

Four year average earnings per share should be around $6.65 at the end of 2021. EPS have grown a little less than 13% annually over the last ten years.

The company is committed to its dividend which has grown to $3.56 (TTM) from around $1.35 in 2014 – so a CAGR of about 17%.

I see analysts estimates (from Zacks) with earnings per share in 2022 around $7 per share. I’m assuming less (between $5 and $5.5) with earnings growth continuing thereafter at an average rate of 13%. Assume the stock trades in 2031 at the current median 7 year PE ratio of 9.4X. EPS will have grown to $15 to $15.50. and the implied price to sell in 2031 would be $144.

You can buy the stock today (if you want) for $72.34. You might get most of that back in dividends and sell the stock for $144 in 2031 for a total return of 13% per year. The NPV of that cash flow is $107 (using an 8% discount rate.) So, at $72.34 PSX is on sale today, at a 31% discount to NPV.

But there’s some things that make me cautious. On the last earnings call, the executive team talked about investments in renewable resources, a battery manufacturing business and converting the gas stations into charging stations for electrical vehicles. They seem to be trying to figure out how to shape the business for a lower carbon future. That’s good. Every business should plan for that. But the lack of a clear plan makes me cautious.

I bought some PSX in April at $59.99. I like it. But not at this price. I put a limit order in today to buy more at $65. If I can get it with that 40% discount/margin of error to the NPV I’ll add to my position. If I can’t, (and btw, these limit orders almost never work for me) then I’ll pass

That’s not much of a pick, but it’s all I have for the Pick of the Week

Current Events: Inflation at the Bagel Shop or “How is inflation like a Jack in the Box? “

The lady in front of us at the bagel shop this morning ordered a dozen bagels. She got twelve. Lady: “Hey, what happened to the baker’s dozen?” Owner: “we had to stop that. You know; inflation.”

Long before anyone had heard of ‘transitory inflation caused by supply-chain issues’ Milton Friedman said this. “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”[1]

I vaguely remember learning something about inflation many years ago in Professor Yahalom’s macroeconomics class. I googled around to refresh and found this:

“We now use the quantity equation to provide us with a theory of long-run inflation. To do so, we use the rules of growth rates. One of these rules is as follows: if you have two variables, x and y, then the growth rate of the product (x × y) is the sum of the growth rate of x and the growth rate of y. We can apply this to the quantity equation:

money supply × velocity of money = price level × real GDP.

“The left side of this equation is the product of two variables, the money supply and the velocity of money. The right side is likewise the product of two variables. So we obtain:

growth rate of the money supply + growth rate of the velocity of money = inflation rate + growth rate of output.

“We have used the fact that the growth rate of the price level is, by definition, the inflation rate.[2]

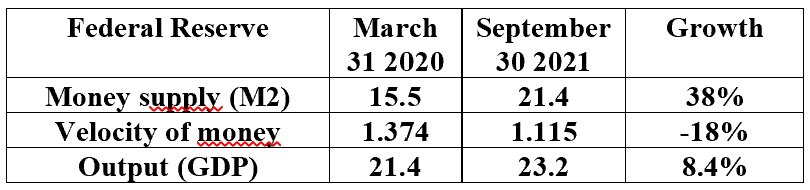

Now let’s look at some data from the Federal Reserve[3]:

38% +(-18%) = Inflation rate +8.4%

20% = Inflation rate + 8.4%

20% - 8.4% = Inflation rate

Inflation rate = 11.6% in the year and a half; so 11.6%/1.5 years = 7.7% annualized?

That’s not too far above the 6% rate we see reported in the news. So far, so good.

There are nine recessions, including the most recent brief 2020 recession, in the Fed’s data set. After most recessions, the velocity of money has increased.

The Fed has announced it will start to stop printing excess money (what I call “starting to stop” the Fed Calls ‘tapering off Quantitative Easing’) sometime in the near future. But for now, the presses are rolling.

And inflation looks quite different if the velocity of money increases back to a pre-pandemic speed. If the growth rate of GDP and money supply don’t change the rate of inflation over the next year and a half will be

growth rate of the money supply + growth rate of the velocity of money = inflation rate + growth rate of output.

38% + (0) = inflation rate + 8.4%

38% - 8.4% = inflation of 29.6

29.6/1.5 years = 19.7% annualized

When you crank up a Jack in the Box you hear a happy tune...until the music stops abruptly and Jack springs up to scare you.

The Fed has been cranking up the money supply since Quantitative Easing 1 following the 2008 recession. There’s a good chance Jack is about to spring out of the box.

(Full Disclosure: everything I learned in college, including macroeconomics, I have forgotten. What I know now I learned on Google yesterday and today. Please feel free to comment, correct or suggest in the comment box below)

[1] Presentation to the Western Economic Association International San Francisco, CA

- John C. Williams, President and CEO, Federal Reserve Bank of San Francisco, July 2, 2012

[2] https://saylordotorg.github.io/text_macroeconomics-theory-through-applications/s15-01-the-quantity-theory-of-money.html

[3] https://fred.stlouisfed.org/series/M2V